The 50/30/20 Budget Rule - How to Split Your Paycheck

The 50/30/20 rule answers the question that kills most budgets before they start: how much should I spend on what? Instead of tracking every purchase into dozens of categories, it divides your after-tax income into three buckets. Fifty percent for needs. Thirty percent for wants. Twenty percent for savings and debt repayment.

Senator Elizabeth Warren introduced the framework in her 2005 book All Your Worth, co-authored with her daughter Amelia Warren Tyagi. Two decades later, it remains the most widely recommended starting point for personal budgeting - not because it is perfect, but because it is simple enough to actually use.

How the Rule Works

Start with your after-tax monthly income - the amount that lands in your bank account after taxes and mandatory deductions. If you earn a regular salary, this is your net paycheck. If you freelance or run a business, subtract 25-30% from gross income for taxes first.

Multiply that number by 0.50, 0.30, and 0.20. Those are your three spending limits.

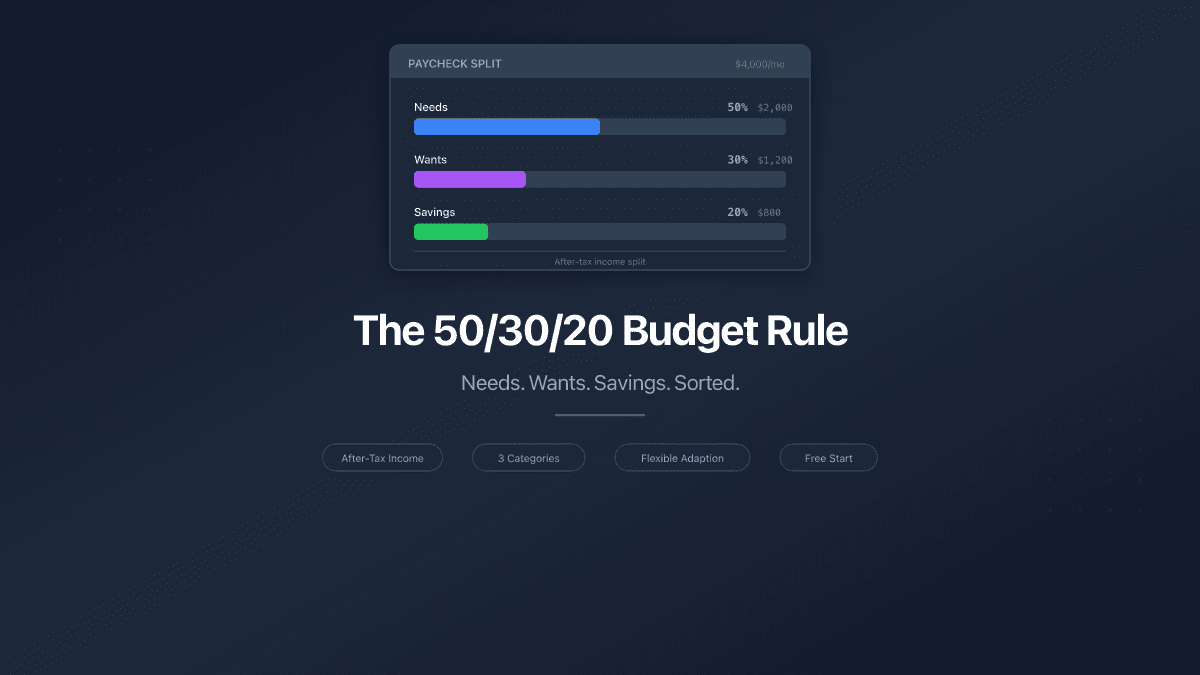

Example on $4,000 after-tax income:

| Category | Percentage | Amount | What goes here |

|---|---|---|---|

| Needs | 50% | $2,000 | Rent, utilities, groceries, insurance, transport, minimum debt payments |

| Wants | 30% | $1,200 | Dining out, entertainment, shopping, subscriptions, hobbies |

| Savings | 20% | $800 | Emergency fund, investments, extra debt payments, retirement |

The rule works on any income level. Earn $3,000? Your needs budget is $1,500. Earn $6,000? It is $3,000. The percentages scale while the discipline stays constant.

50% - Needs: What Counts and What Does Not

Needs are expenses you cannot eliminate without serious consequences. Miss rent and you lose housing. Skip groceries and you do not eat. Cancel health insurance and one medical bill can create years of debt.

Always needs:

- Rent or mortgage payments

- Utilities (electricity, water, gas, internet)

- Groceries (food you cook at home, not restaurants)

- Transportation (car payment, fuel, insurance, public transit pass)

- Health insurance and essential medication

- Minimum debt payments (credit card minimums, student loan minimums)

- Childcare (if required for work)

Never needs (even if they feel like it):

- Streaming services

- Gym memberships

- Dining out

- Premium phone plans beyond basic service

- Brand-name groceries when generic versions exist

The line between needs and wants is personal, but the test is simple: would your life function without it? If yes, it is a want.

Groceries are a need. The difference between buying store-brand pasta for $1.20 and artisan pasta for $4.50 is a want. The category is "need" but individual purchase decisions within it can contain want-spending. Be honest about where the line falls for you.

30% - Wants: Spending Without Guilt

Wants make life enjoyable. The 50/30/20 rule does not ask you to eliminate them - it gives them a defined budget so you can spend without guilt.

Common wants:

- Restaurants, cafes, food delivery

- Entertainment (concerts, movies, games, streaming)

- Shopping beyond basics (clothing you want, not clothing you need)

- Hobbies and sports (gym, classes, equipment)

- Travel and vacations

- Subscription services (streaming, magazines, apps)

- Upgrades (premium phone plan, faster internet, nicer car)

Thirty percent sounds generous until you total it up. On $4,000 take-home pay, you have $1,200 for wants. Four restaurant meals at $60, two streaming services at $15 each, a gym at $50, a couple of shopping purchases, and a weekend trip eat through that budget faster than expected.

This is where tracking matters most. Needs are predictable - rent is the same every month. Wants fluctuate and expand silently.

20% - Savings and Debt Repayment

The 20% bucket builds your financial future. This is the money that separates "getting by" from "getting ahead."

Priority order:

- Emergency fund - three to six months of essential expenses. This comes first because without it, any unexpected cost (car repair, medical bill, job loss) forces you into debt.

- High-interest debt - credit cards, personal loans above 8-10% interest. Every dollar here saves you interest.

- Retirement savings - employer match first (free money), then additional contributions.

- Other investments - index funds, brokerage accounts, real estate down payment savings.

If you carry high-interest debt, the 20% bucket targets that aggressively. Once debt is cleared, the same 20% shifts to savings and investments. The habit stays; the destination changes.

The 20% is a minimum, not a ceiling. If your needs cost less than 50% of income, redirect the surplus to savings rather than inflating your wants budget. The faster you build financial reserves, the more options you have.

When 50% Is Not Enough for Needs

The 50/30/20 rule was designed for the average American household in 2005. Housing costs have risen significantly since then. In many cities, rent alone consumes 30-40% of after-tax income, leaving little room for other needs within the 50% limit.

If your needs exceed 50%, do not abandon budgeting. Adjust the percentages:

| Situation | Adjusted split | Strategy |

|---|---|---|

| Housing is 35%+ of income | 60/20/20 | Reduce wants, protect savings |

| High-cost city | 65/15/20 | Aggressive want-cutting, maintain savings |

| Debt-heavy period | 50/20/30 | Shift want-money to debt repayment temporarily |

| Low income, high essentials | 70/20/10 | Save what you can, increase income as priority |

| Dual income, low housing costs | 40/30/30 | Accelerate savings and investments |

The key insight: keep savings above 10% regardless. Below that, you accumulate no financial cushion and one unexpected expense creates a debt spiral.

If your needs consistently exceed 70% of income, the problem is structural - not a budgeting failure. Consider whether a housing change, income increase, or debt consolidation would create more breathing room than tighter tracking alone.

Track Your 50/30/20 Split in Practice

The rule is useless without tracking. You need to know where each dollar goes - not in theory, but in actual monthly spending.

Step 1: Set up three top-level categories.

In PaperLink, create or use existing categories that map to the three buckets. The 100+ pre-built categories already cover common expenses - group them mentally into needs, wants, and savings.

Step 2: Record every transaction.

Each purchase gets categorized as it happens. PaperLink's autocomplete learns your patterns - after a few entries, "Whole Foods" auto-fills as Groceries (needs), "Netflix" auto-fills as Subscriptions (wants).

Step 3: Review monthly.

At month-end, filter by category and total each bucket. Compare against your targets. Did needs stay under 50%? Did wants creep above 30%? Is savings hitting 20%?

The first month is diagnostic. Do not try to hit perfect percentages immediately. Observe where you actually stand, then adjust spending over the next two to three months to move toward the target split.

For a complete beginner's guide to budgeting - including how to choose between 50/30/20, envelope budgeting, and zero-based budgeting - read our pillar guide.

FAQ

Is the 50/30/20 rule based on after-tax or gross income?

After-tax. Use your net paycheck - the amount deposited into your bank account. For freelancers, estimate your tax obligation (typically 25-30%) and subtract it from gross income before applying the percentages.

What if I cannot save 20%?

Start where you are. Even 5% is better than 0%. The goal is to build the habit of paying yourself first. As income grows or debts decrease, gradually increase toward 20%.

Does the 50/30/20 rule work for couples?

Yes. Combine both after-tax incomes and apply the rule to the total household income. This often works better than individual budgets because shared housing costs become a smaller percentage of combined income.

Should I include debt minimum payments in needs or savings?

Minimum payments are needs - you must pay them. Extra payments beyond the minimum go in the savings/debt bucket. This distinction matters because it shows the true cost of carrying debt: it reduces your needs budget.

Start Splitting Your Paycheck

The 50/30/20 rule is not the only budgeting method, but it is the easiest to start with. Three categories. Three percentages. One monthly check-in.

Create your free account and set up your 50/30/20 categories in under a minute. Pre-configured expense categories are included - start tracking your split today.

PaperLink goes beyond budgeting. Share business proposals, invoices, and presentations with built-in analytics - see who viewed your documents, which pages held their attention, and how long they spent reading. Explore document sharing analytics.

Related articles:

- How to Budget - A Complete Beginner's Guide - the full guide to budgeting methods, categories, and tools

- Free Expense Tracker - PaperLink's built-in expense tracking features

- Freelancer Finance Guide - budgeting with irregular income

Bereit, PaperLink auszuprobieren?

Erstellen Sie Rechnungen, teilen Sie Dokumente und verwalten Sie Ihr Unternehmen — alles an einem Ort.

Ähnliche Beiträge

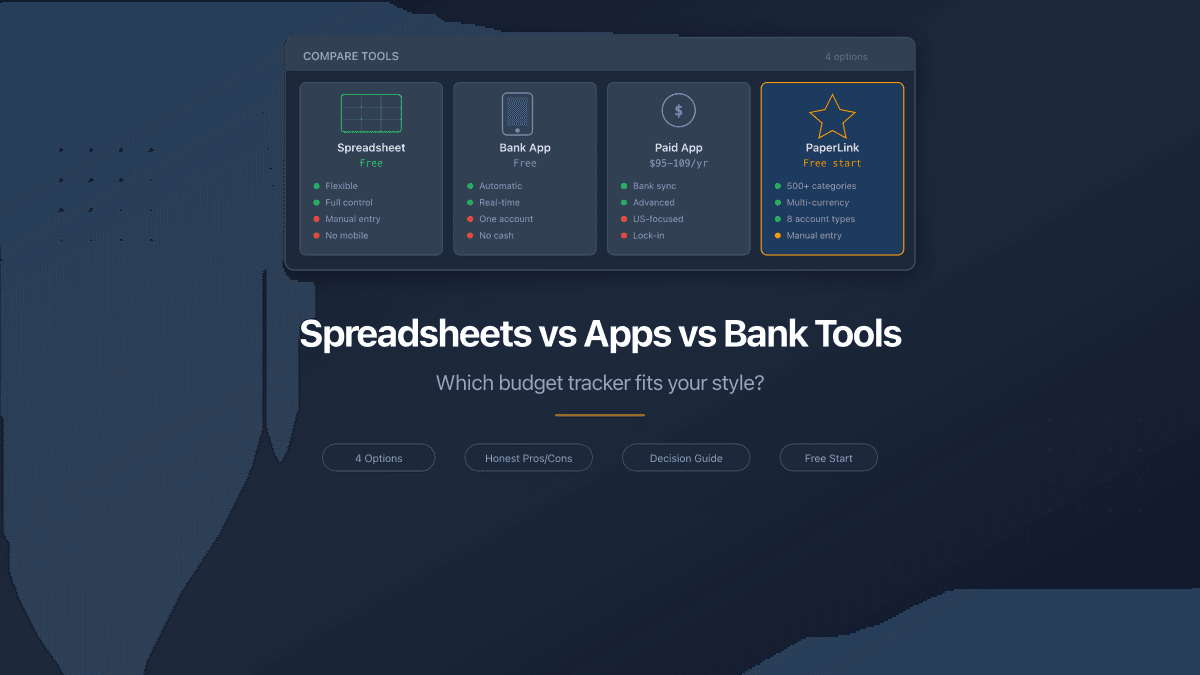

Spreadsheets vs Apps vs Bank Tools - Where to Track Money

Spreadsheets, bank apps, and dedicated budget tools compared honestly. Pros, cons, pricing, and which option fits your situation in 2026.

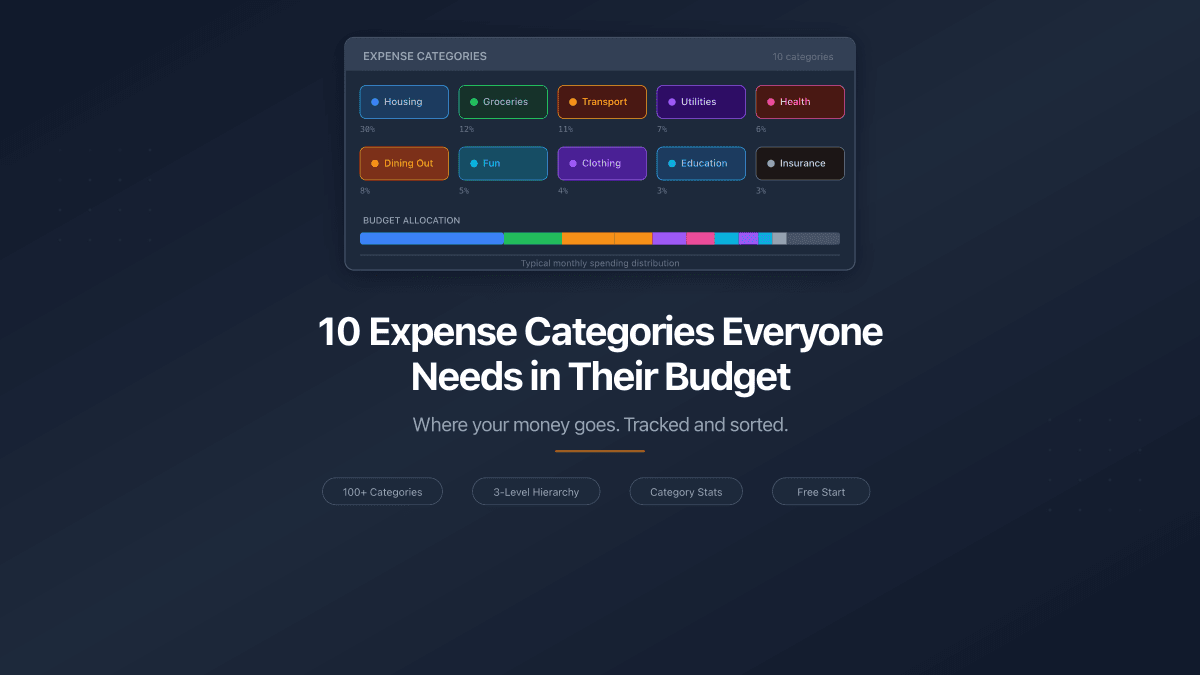

10 Expense Categories Everyone Needs in Their Budget

The 10 expense categories that cover 95% of personal spending. Typical budget share for each, example expenses, and one practical way to reduce costs.

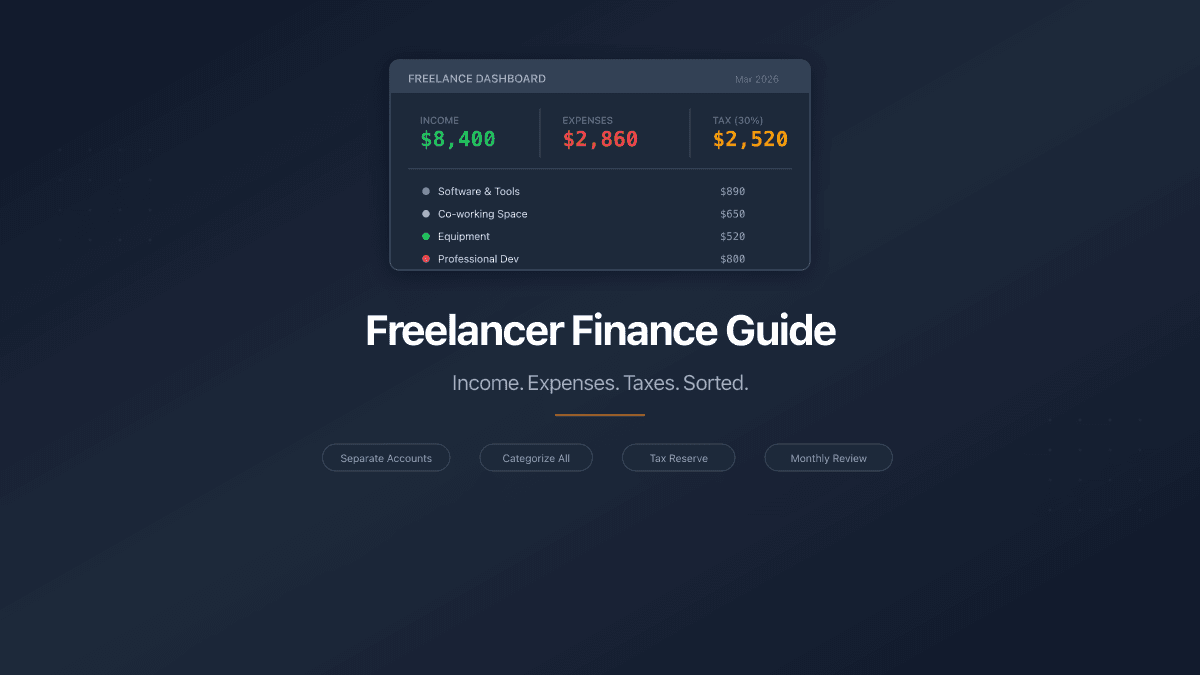

Freelancer Finance Guide - Track Income, Expenses, and Taxes

A practical guide to freelancer finances: separate accounts, categorize expenses, set aside 25-30% for taxes, and review monthly. Free tools included.